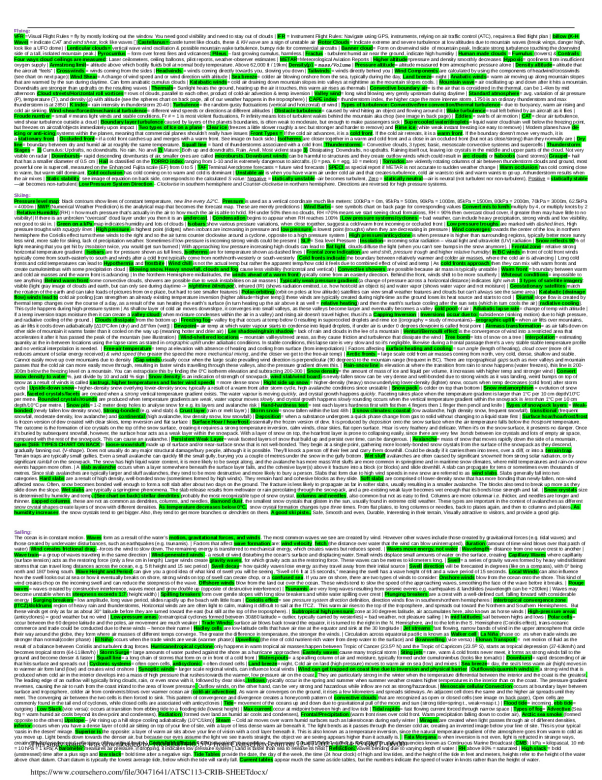

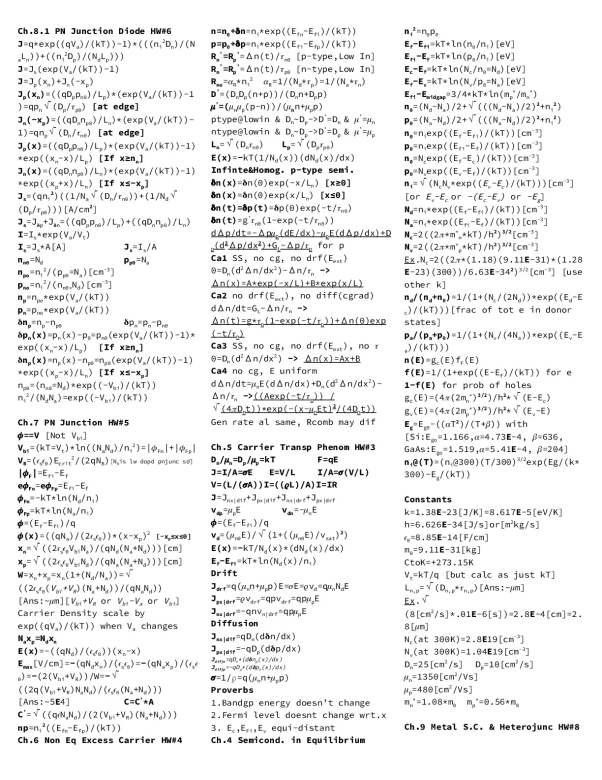

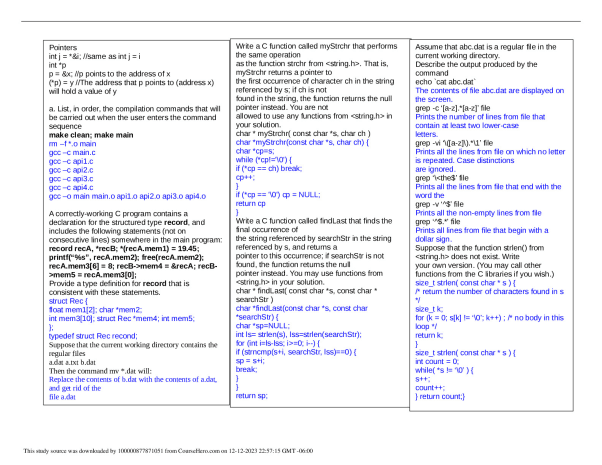

San Jose State University

BUS1 123A

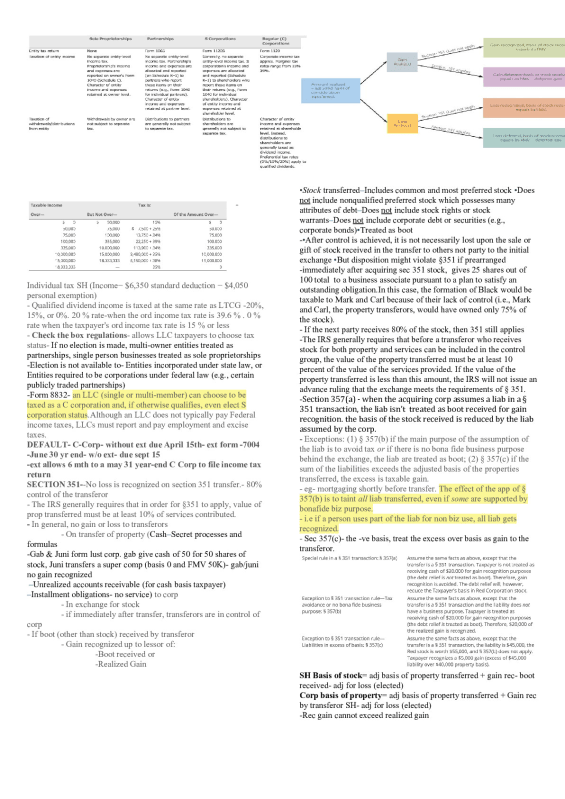

•Stock transferred–Includes common and most preferred stock •Does not include nonqualified preferred stock which possesses many attributes of debt–Does not include stock rights or stock warrants–Does not include corporate debt or securities (e.g., corporate bonds)•Treated as boot -•After control is achieved, it is not necess

...[Show More]

•Stock transferred–Includes common and most preferred stock •Does not include nonqualified preferred stock which possesses many attributes of debt–Does not include stock rights or stock warrants–Does not include corporate debt or securities (e.g., corporate bonds)•Treated as boot -•After control is achieved, it is not necessarily lost upon the sale or gift of stock received in the transfer to others not party to the initial exchange •But disposition might violate §351 if prearranged -immediately after acquiring sec 351 stock, gives 25 shares out of 100 total to a business associate pursuant to a plan to satisfy an outstanding obligation.In this case, the formation of Black would be taxable to Mark and Carl because of their lack of control (i.e., Mark and Carl, the property transferors, would have owned only 75% of the stock). - If the next party receives 80% of the stock, then 351 still applies -The IRS generally requires that before a transferor who receives stock for both property and services can be included in the control group, the value of the property transferred must be at least 10 percent of the value of the services provided. If the value of the property transferred is less than this amount, the IRS will not issue an advance ruling that the exchange meets the requirements of § 351. -Section 357(a) - when the acquiring corp assumes a liab in a § 351 transaction, the liab isn’t treated as boot received for gain recognition. the basis of the stock received is reduced by the liab assumed by the corp. - Exceptions: (1) § 357(b) if the main purpose of the assumption of the liab is to avoid tax or if there is no bona fide business purpose behind the exchange, the liab are treated as boot; (2) § 357(c) if the sum of the liabilities exceeds the adjus

[Show Less]

-preview.png)

-preview.png)