McMaster University

COMMERCE 3FA3

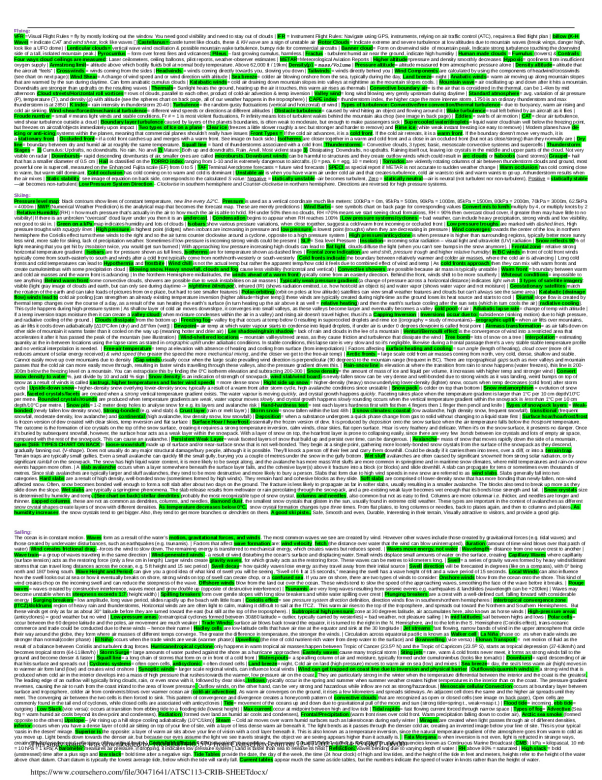

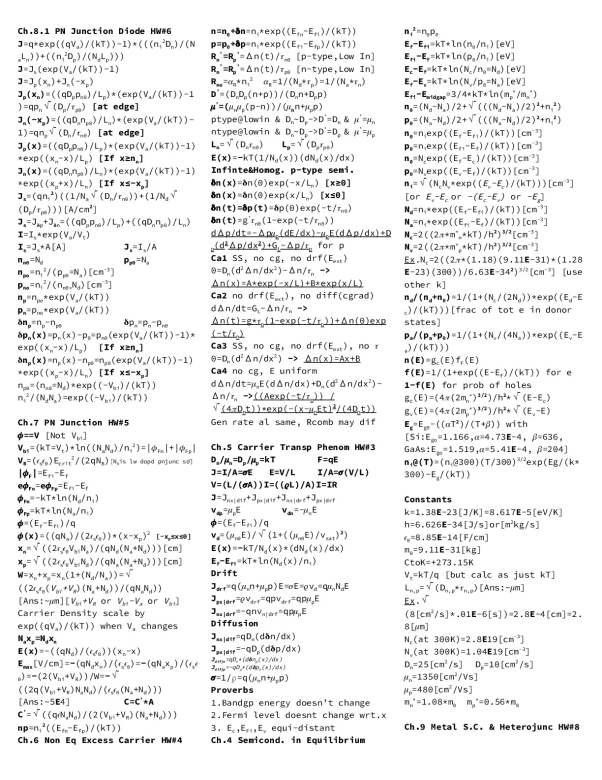

Chapter 14 – Cost of Capital *RR = 10% - Firms must earn 10% on investment to compensate investors for the use of capital they gave to finance the project *Cost of capital for Bo = risk free rate *Cost of capital depends on the risk of the investment ROE = Net income after income and taxes divided by average shareholders equity Cost of equity �

...[Show More]

Chapter 14 – Cost of Capital *RR = 10% - Firms must earn 10% on investment to compensate investors for the use of capital they gave to finance the project *Cost of capital for Bo = risk free rate *Cost of capital depends on the risk of the investment ROE = Net income after income and taxes divided by average shareholders equity Cost of equity – return that equity investors require on their investment in the firm 1) Dividend growth model: PV of all future dividends - get the stock price at any point in time, Pros: simple, cons: only applicable if currently paying div; need const growth rate; doesn’t consider risk; sensitive to est growth rate Constant growth: D1 = Do x (1+g) Cost of equity: Re = (D1/ Po) + g ? = బ×(ଵା) ோି ?௧ = ×(ଵା) ି = శభ ି Grows at constant rate after some time Dt = Do x (1+g)T Po: price/share of stock today Dividend: div/share in 1 year k:expected rate of return – discount rate g: growth rate of company (future) General case: price today of share of stock is the OV of all its future div Po = E D/ (1+r)1 + D/(1+r)2 + D/(1+r)3…. Estimating growth: g = (1- Payout Ratio)(ROE) Earnings next year: earnings this year + RE this year x return on Re (1-Payout Ratio) = Retention Ratio g = Retention ratio x ROE Retention ratio = Re / net income DDM Zero growth rate: constant dividend Perpetuity: ? = భ Return on equity = net income after interest and taxes/ avg. common SH equity 2. SML Approach E (Re) – Rf + Be x [E(Rm) – Rf] RR: (Re) = Rf + Be x [Rm – Rf] Market risk premium: E[Rm] – Rf * Assumes future risks are similar to past risks; applies to firms that retain all earnings B = beta of stock Rf = risk free rate Rm = Expected mkt return Expected return – return on any risky asset expected in the future Reduction of Rf will increase a firm’s cost of equity Cost of debt = YTM – return lenders require on the firm’s debt – NOT the coupon rate (unless face val and mkt val of debt (bond) are the same) Cost of preferred stock – perpetuity: Rp = D/Po D = fixed dividend Po = current price/ share of the preferred stock WACC – required return on our assets based on the market’s perceptions of the risk of those assets Capital structure weights E = mkt value of equity: # O/S shares x price/share D = mkt value of debt = # O/S bonds x bond price V = mkt value of the firm = D + E D/E = 0.35/1 D = 0.35; E = 1; V = 1.35 cost of preferred equity: Rp = (rate x face value) / share price Target capital structure = D / E * weights are based on mkt val of firm’s debt and equity Weights : We = E/V = % financed with equity Wd = D/V = % financed with debt Taxes and WACC – we are concerned with after tax cash flows Pre tax cost of debt: is based on the current YTM of the firm’s O/S bonds * After tax cost of debt = Rd (1 – Tc) WACC = (E/V) Re + (D/V) Rd (1 -Tc) ??? = −? + ?ଵ 1 + ? + ?ଶ (1 + ?) ଶ + ⋯ + ?௧ (1 + ?) ௧ If we use WACC for all projects: 1. Rejects profitable projects with risks less than those of the overall firm 2. Makes unprofitable investments with risks > overall firm. 3. Increases the overall risk overtime Pure play approach – used WACC that unique to a particular project, find one or more companies that specialize in the product or service – compute beta for each company and take the average. Return for that risk = Beta with CAPM Subjective Approach: consider the project’s risk relative to the overall, if the project is more risky that the firm, use a discount rate greater than the WACC OR if the project is less risky that the firm, use a discount rate less than the WACC – reduce error rate Company valuation: CFA = EBIT (1 – Tc) + Dep – Change in NWC – Capital spending If CFA is expected to grow at a const. rate g forever; firm value: Vt = CFA*t +1 / WACC -g Flotation cost, WAFC = (E/V) x fe + (D/V) x Fd *True cost: Capital investment / (1-f) *NPV = PV of future cash flows – True cost WAFC (for internal equity), fa = (D/V) x Fd The Huff Co. has just gone public. Under a firm commitment agreement, Huff received $22.50 for each of the 6 million shares sold. The initial offering price was $23.65 per share, and the stock rose to $25.42 per share in the first few minutes of trading. Huff paid $5,225,500 in direct legal and other costs, and $190,000 in indirect costs. The flotation costs were what percentage of the funds raised? Net amount raised = 6m ($22.50) = $135,000,000; Total direct costs = $5,225,500 + ($23.65 - $22.50) (6m) = $12,125,500; Total indirect costs = $190,000 + ($25.42 - $23.65) (6m) = $10,810,000; Total costs = $8,160,000 + $10,810,000 = $22,935,500Flotation cost% = $22,935,500/$135,000,000 = 17.73% PVSimple = F (1+ Kn) n PVCompounding = ி (ଵା) PVContinuous = ி ೖ∗ Perp: A???: ? ቂଵି భ (భ

[Show Less]

-preview.png)

-preview.png)