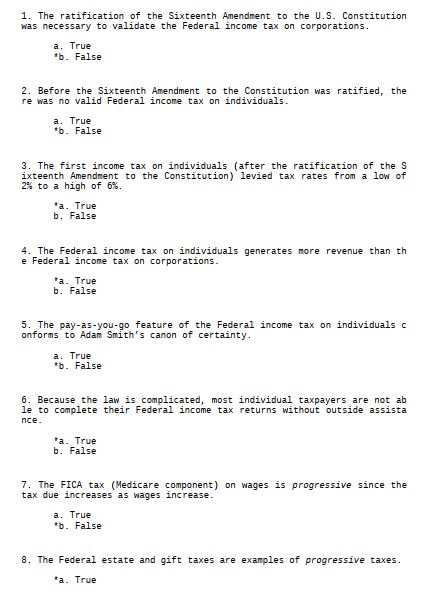

Strayer UniversityACC 307 2014 37th Test BankFIRST 100 QUESTIONS AND ANSWERS1. The ratification of the Sixteenth Amendment to the U.S. Constitutionwas necessary to validate the Federal income tax on corporations.a. True*b. False2. Before the Sixteenth Amendment to the Constitution was ratified, there was no valid Federal income tax on individuals.a. True*b. False3. The first income tax on individ

...[Show More]

FIRST 100 QUESTIONS AND ANSWERS

1. The ratification of the Sixteenth Amendment to the U.S. Constitution

was necessary to validate the Federal income tax on corporations.

a. True

*b. False

2. Before the Sixteenth Amendment to the Constitution was ratified, the

re was no valid Federal income tax on individuals.

a. True

*b. False

3. The first income tax on individuals (after the ratification of the S

ixteenth Amendment to the Constitution) levied tax rates from a low of

2% to a high of 6%.

*a. True

b. False

4. The Federal income tax on individuals generates more revenue than th

e Federal income tax on corporations.

*a. True

b. False

5. The pay-as-you-go feature of the Federal income tax on individuals c

onforms to Adam Smith’s canon of certainty.

a. True

*b. False

6. Because the law is complicated, most individual taxpayers are not ab

le to complete their Federal income tax returns without outside assista

nce.

*a. True

b. False

7. The FICA tax (Medicare component) on wages is progressive since the

tax due increases as wages increase.

a. True

*b. False

8. The Federal estate and gift taxes are examples of progressive taxes.

*a. True

b. False

9. The Federal excise tax on cigarettes is an example of a proportional

tax.

*a. True

b. False

10. Currently, the Federal income tax is less progressive than it ever

has been in the past.

a. True

*b. False

11. Mona inherits her mother’s personal residence, which she converts t

o a furnished rent house. These changes should affect the amount of ad

valorem property taxes levied on the properties.

*a. True

b. False

12. A fixture will be subject to the ad valorem tax on personalty rathe

r than the ad valorem tax on realty.

a. True

*b. False

13. Even if property tax rates are not changed, the amount of ad valore

m taxes imposed on realty may not remain the same.

*a. True

b. False

14. The ad valorem tax on personal use personalty is more often avoided

by taxpayers than the ad valorem tax on business use personalty.

*a. True

b. False

15. A Federal excise tax is no longer imposed on admission to theaters.

*a. True

b. False

16. There is a Federal excise tax on hotel occupancy.

a. True

*b. False

17. The Federal gas-guzzler tax applies only to automobiles manufacture

d overseas and imported into the U.S.

a. True

*b. False

18. Like the Federal counterpart, the amount of the state excise taxes

on gasoline varies from state to state.

a. True

*b. False

19. Not all of the states that impose a general sales tax also have a u

se tax.

a. True

*b. False

20. Sales made by mail order are not exempt from the application of a g

eneral sales (or use) tax.

*a. True

b. False

21. Two persons who live in the same state but in different counties ma

y not be subject to the same general sales tax rate.

*a. True

b. False

22. States impose either a state income tax or a general sales tax, but

not both types of taxes.

a. True

*b. False

23. A safe and easy way for a taxpayer to avoid local and state sales t

axes is to make the purchase in a state that levies no such taxes.

a. True

*b. False

24. On transfers by death, the Federal government relies on an estate t

ax, while states impose an estate tax, an inheritance tax, both taxes,

or neither tax.

*a. True

b. False

25. An inheritance tax is a tax on a decedent’s right to pass property

at death.

a. True

*b. False

26. One of the major reasons for the enactment of the Federal estate ta

x was to prevent large amounts of wealth from being accumulated within

the family unit.

*a. True

b. False

27. Under Clint’s will, all of his property passes to either the Luther

an Church or to his wife. No Federal estate tax will be due on Clint’s

death in 2013.

*a. True

b. False

28. Under the usual state inheritance tax, two heirs, a cousin and a so

n of the deceased, would not be taxed at the same rate.

*a. True

b. False

29. The annual exclusion, currently $14,000, is available for gift and

estate tax purposes.

a. True

*b. False

30. In 2012, José, a widower, sells land (fair market value of $100,00

0) to his daughter, Linda, for $50,000. José has made a taxable gift of

$50,000.

a. True

*b. False

31. Julius, a married taxpayer, makes gifts to each of his six children.

A maximum of twelve annual exclusions could be allowed as to these gif

ts.

*a. True

b. False

32. One of the motivations for making a gift is to save on income taxes.

*a. True

b. False

33. The formula for the Federal income tax on corporations is the same

as that applicable to individuals.

a. True

*b. False

34. A state income tax can be imposed on nonresident taxpayers who earn

income within the state or on an itinerant basis.

*a. True

b. False

35. For state income tax purposes, a majority of states allow a deducti

on for Federal income taxes.

a. True

*b. False

36. Some states use their state income tax return as a means of collect

ing unpaid sales and use taxes.

*a. True

b. False

37. No state has offered an income tax amnesty program more than once.

a. True

*b. False

38. For Federal income tax purposes, there never has been a general amn

esty period.

*a. True

b. False

39. Under state amnesty programs, all delinquent and unpaid income taxe

s are forgiven.

a. True

*b. False

40. When a state decouples from a Federal tax provision, it means that

this provision will not apply for state income tax purposes.

*a. True

b. False

41. The principal objective of the FUTA tax is to provide some measure

of retirement security.

a. True

*b. False

42. Currently, the tax base for the Social Security component of the FI

CA is not limited to a dollar amount.

a. True

*b. False

43. A parent employs his twin daughters, age 17, in his sole proprietor

ship. The daughters are not subject to FICA coverage.

*a. True

b. False

44. Unlike FICA, FUTA requires that employers comply with state as well

as Federal rules.

*a. True

b. False

45. A major advantage of a flat tax type of income tax is its simplicit

y.

*a. True

b. False

46. The value added tax (VAT) has not had wide acceptance in the intern

ational community.

a. True

*b. False

47. If more IRS audits are producing a greater number of no change resu

lts, this indicates increased compliance on the part of taxpayers.

a. True

*b. False

48. The amount of a taxpayer’s itemized deductions will increase the ch

ance of being audited by the IRS.

*a. True

b. False

49. In an office audit, the audit by the IRS takes place at the office

of the taxpayer.

a. True

*b. False

50. The IRS agent auditing the return will issue an RAR even if the tax

payer owes no additional taxes.

*a. True

b. False

51. If a “special agent” becomes involved in the audit of a return, thi

s indicates that the IRS suspects that fraud is involved.

*a. True

b. False

52. If a taxpayer files early (i.e., before the due date of the return),

the statute of limitations on assessments begins on the date the retur

n is filed.

a. True

*b. False

53. For omissions from gross income in excess of 25% of that reported,

there is no statute of limitations on additional income tax assessments

by the IRS.

a. True

*b. False

54. If an income tax return is not filed by a taxpayer, there is no sta

tute of limitations on assessments of tax by the IRS.

*a. True

b. False

55. If fraud is involved, there is no time limit on the assessment of a

deficiency by the IRS.

*a. True

b. False

56. The IRS is required to redetermine the interest rate on underpaymen

ts and overpayments once a year.

a. True

*b. False

57. A calendar year taxpayer files his 2012 Federal income tax return o

n March 5, 2013. The return reflects an overpayment of $6,000, and the

taxpayer requests a refund of this amount. The refund is paid on May 17,

2013. The refund need not include interest.

*a. True

b. False

58. For individual taxpayers, the interest rate for income tax refunds

(overpayments) is the same as that applicable to assessments (underpaym

ents).

*a. True

b. False

59. During any month in which both the failure to file penalty and the

failure to pay penalty apply, the failure to file penalty is increased

by the amount of the failure to pay penalty.

a. True

*b. False

60. When interest is charged on a deficiency, any part of a month count

s as a full month.

a. True

*b. False

61. For the negligence penalty to apply, the underpayment must be cause

d by intentional disregard of rules and regulations without intent to d

efraud.

*a. True

b. False

62. Upon audit by the IRS, Faith is assessed a deficiency of $40,000 of

which $25,000 is attributable to negligence. The 20% negligence penalty

will apply to $25,000.

*a. True

b. False

63. If the tax deficiency is attributable to fraud, the negligence pena

lty will not be imposed.

*a. True

b. False

64. The civil fraud penalty can entail large fines and possible incarce

ration.

a. True

*b. False

65. Even though a client refuses to correct an error on a past return,

it may be possible for a practitioner to continue to prepare returns fo

r the client.

*a. True

b. False

66. In preparing an income tax return, the use of a client’s estimates

is not permitted.

a. True

*b. False

67. In preparing a tax return, all questions on the return must be answ

ered.

a. True

*b. False

68. A CPA firm in California sends many of its less complex tax returns

to be prepared by a group of accountants in India. If certain procedure

s are followed, this outsourcing of tax return preparation is proper.

*a. True

b. False

69. The objective of pay-as-you-go (paygo) is to achieve revenue neutra

lity.

*a. True

b. False

70. When Congress enacts a tax cut that is phased in over a period of y

ears, revenue neutrality is achieved.

a. True

*b. False

71. A tax cut enacted by Congress that contains a sunset provision will

make the tax cut temporary.

*a. True

b. False

72. The tax law provides various tax credits, deductions, and exclusion

s that are designed to encourage taxpayers to obtain additional educati

on. These provisions can be justified on both economic and equity groun

ds.

a. True

*b. False

73. Various tax provisions encourage the creation of certain types of r

etirement plans. Such provisions can be justified on both economic and

social grounds.

*a. True

b. False

74. To lessen, or eliminate, the effect of multiple taxation, a taxpaye

r who is subject to both foreign and U.S. income taxes on the same inco

me is allowed either a deduction or a credit for the foreign tax paid.

*a. True

b. False

75. To mitigate the effect of the annual accounting period concept, the

tax law permits the carryforward to other years of the excess charitabl

e contributions of a particular year.

*a. True

b. False

76. Jason’s business warehouse is destroyed by fire. As the insurance p

roceeds exceed the basis of the property, a gain results. If Jason shor

tly reinvests the proceeds in a new warehouse, no gain is recognized du

e to the application of the wherewithal to pay concept.

*a. True

b. False

77. As it is consistent with the wherewithal to pay concept, the tax la

w requires a seller to recognize gain in the year the installment sale

occurs.

a. True

*b. False

78. Stealth taxes have the effect of generating additional taxes from a

ll taxpayers.

a. True

*b. False

79. A provision in the law that compels accrual basis taxpayers to pay

a tax on prepaid income in the year received and not when earned is con

sistent with generally accepted accounting principles.

a. True

*b. False

80. As a matter of administrative convenience, the IRS would prefer to

have Congress decrease (rather than increase) the amount of the standar

d deduction allowed to individual taxpayers.

a. True

*b. False

81. In cases of doubt, courts have held that tax relief provisions shou

ld be broadly construed in favor of taxpayers.

a. True

*b. False

82. On occasion, Congress has to enact legislation that clarifies the t

ax law in order to change a result reached by the U.S. Supreme Court.

*a. True

b. False

83. Which, if any, of the following statements best describes the histo

ry of the Federal income tax?

a. It did not exist during the Civil War.

*b. The Federal income tax on corporations was held by the U.S. S

upreme Court to be allowable under the U.S. Constitution.

c. The Federal income tax on individuals was held by the U.S. Sup

reme Court to be allowable under the U.S. Constitution.

d. Both the Federal income tax on individuals and on corporations

was held by the U.S. Supreme Court to be contrary to the U.S. Con

stitution.

e. None of the above.

84. Which, if any, is not one of Adam Smith’s canons of taxation?

a. Economy.

b. Certainty.

c. Convenience.

*d. Simplicity.

e. Equality.

85. Which, if any, of the following taxes are proportional (rather than

progressive)?

*a. State general sales tax.

b. Federal corporate income tax.

c. Federal estate tax.

d. Federal gift tax.

e. All of the above.

86. Which, if any, of the following transactions will increase a taxing

jurisdiction’s revenue from the ad valorem tax imposed on real estate?

a. A resident dies and leaves his farm to his church.

b. A large property owner issues a conservation easement as to so

me of her land.

*c. A tax holiday issued 10 years ago has expired.

d. A bankrupt motel is acquired by the Red Cross and is to be use

d to provide housing for homeless persons.

e. None of the above.

87. Which, if any, of the following transactions will decrease a taxing juri

sdiction’s ad valorem tax revenue imposed on real estate?

*a. A tax holiday is granted to an out-of-state business that is

searching for a new factory site.

b. An abandoned church is converted to a restaurant.

c. A public school is razed and turned into a city park.

d. A local university sells a dormitory that will be converted fo

r use as an apartment building.

e. None of the above.

88. Which, if any, of the following is a typical characteristic of an a

d valorem tax on personalty?

a. Taxpayer compliance is greater for personal use property than

for business use property.

*b. The tax on automobiles sometimes considers the age of the veh

icle.

c. Most states impose a tax on intangibles.

d. The tax on intangibles generates considerable revenue since it

is difficult for taxpayers to avoid.

e. None of the above.

89. Federal excise taxes that are no longer imposed include:

a. Tax on air travel.

b. Tax on wagering.

c. Tax on the manufacture of sporting equipment.

d. Tax on alcohol.

*e. None of the above.

90. Taxes not imposed by the Federal government include:

a. Tobacco excise tax.

b. Customs duties (tariffs on imports).

*c. Tax on rent cars.

d. Gas guzzler tax.

e. None of the above.

91. Taxes levied by both states and the Federal government include:

a. General sales tax.

b. Custom duties.

c. Hotel occupancy tax.

d. Franchise tax.

*e. None of the above.

92. Taxes levied by all states include:

*a. Tobacco excise tax.

b. Individual income tax.

c. Inheritance tax.

d. General sales tax.

e. None of the above.

93. A use tax is imposed by:

a. The Federal government and all states.

b. The Federal government and a majority of the states.

c. All states and not the Federal government.

*d. Most of the states and not the Federal government.

e. None of the above.

94. Burt and Lisa are married and live in a common law state. Burt want

s to make gifts to their four children in 2013. What is the maximum amo

unt of the annual exclusion they will be allowed for these gifts?

a. $14,000.

b. $28,000.

c. $56,000.

*d. $112,000.

e. None of the above.

95. Property can be transferred within the family group by gift or at d

eath. One motivation for preferring the gift approach is:

a. To take advantage of the higher unified transfer tax credit av

ailable under the gift tax.

b. To avoid a future decline in value of the property transferred

*c. To take advantage of the per donee annual exclusion.

d. To shift income to higher bracket donees.

e. None of the above.

96. Indicate which, if any, statement is incorrect. State income taxes:

a. Can piggyback to the Federal version.

*b. Cannot apply to visiting nonresidents.

c. Can decouple from the Federal version.

d. Can provide occasional amnesty programs.

e. None of the above.

97. State income taxes generally can be characterized by:

*a. The same date for filing as the Federal income tax.

b. No provision for withholding procedures.

c. Allowance of a deduction for Federal income taxes paid.

d. Applying only to individuals and not applying to corporations.

e. None of the above.

98. A characteristic of FICA is that:

a. It does not apply when one spouse works for the other spouse.

b. It is imposed only on the employer.

c. It provides a modest source of income in the event of loss of

employment.

d. It is administered by both state and Federal governments.

*e. None of the above.

99. A characteristic of FUTA is that:

a. It is imposed on both employer and employee.

b. It is imposed solely on the employee.

*c. Compliance requires following guidelines issued by both state

and Federal regulatory authorities.

d. It is applicable to spouses of employees but not to any childr

en under age 18.

e. None of the above.

100. The U.S. (either Federal, state, or local) does not impose:

a. Franchise taxes.

b. Severance taxes.

c. Occupational fees.

d. Custom duties.

*e. Export duties.

[Show Less]

-preview.jpeg)