Chapter 17 Audit Sampling for Test of Controls 1. What are the test of controls audit procedure in general, and what purpose do they serve? 2. In test of controls auditing, why is it necessary to define a compliance deviation in advance? Give seven examples of compliance deviations. 3. Which judgments must an auditor make when deciding on a sample size for test o

...[Show More]

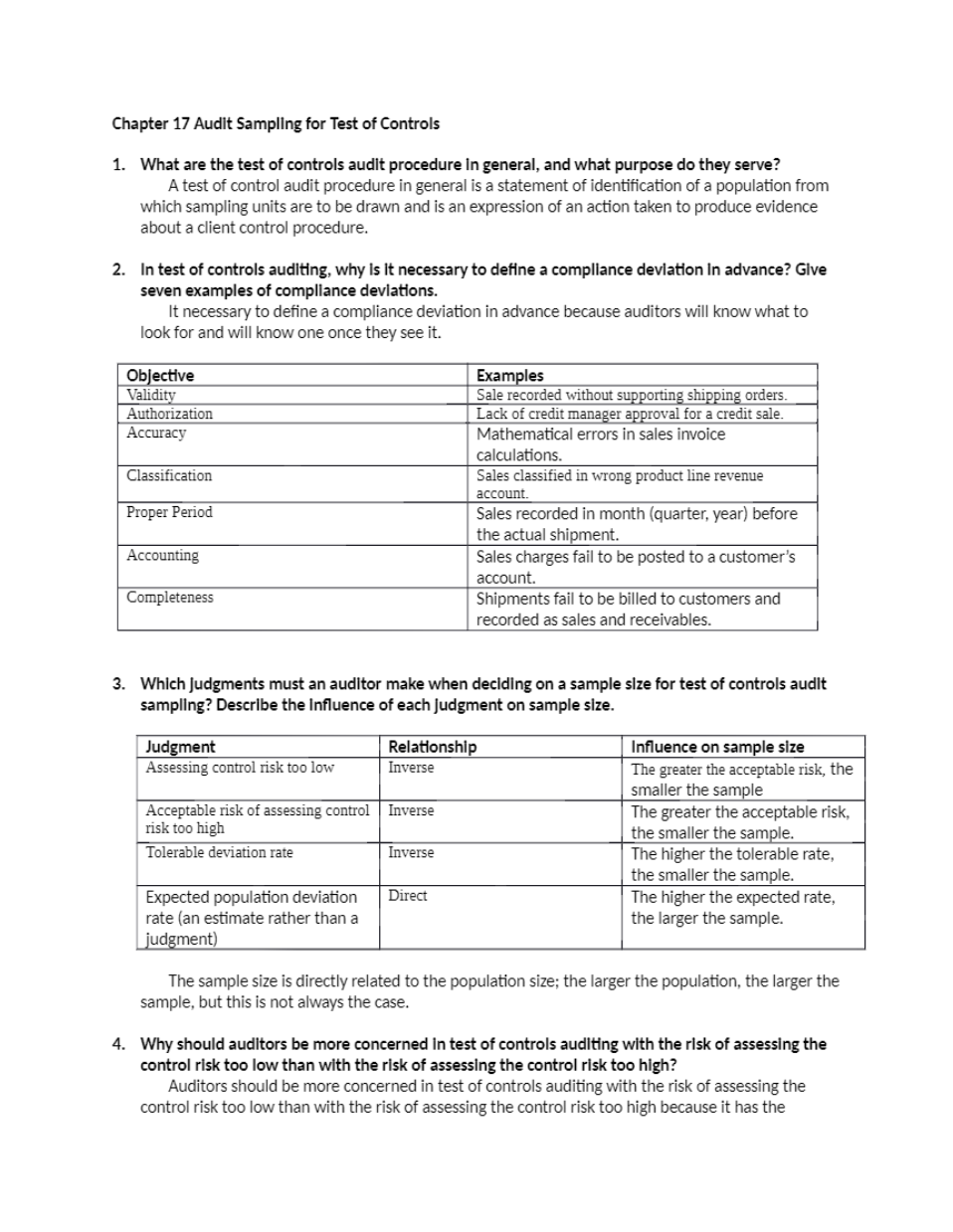

Chapter 17 Audit Sampling for Test of Controls

1. What are the test of controls audit procedure in general, and what purpose do they serve?

2. In test of controls auditing, why is it necessary to define a compliance deviation in advance? Give seven examples of compliance deviations.

3. Which judgments must an auditor make when deciding on a sample size for test of controls audit sampling? Describe the influence of each judgment on sample size.

4. Why should auditors be more concerned in test of controls auditing with the risk of assessing the control risk too low than with the risk of assessing the control risk too high?

5. Write the expanded risk model. What risk is implied for “test for detail risk” when: inherent risk = 1.0, control risk = 0.40, analytical procedures risk = 0.60, audit risk = 0.048, tolerable misstatement = P10, 000, and the estimated standard deviation in the population = P25?

6. What is the connection between possible assessments of control risk and a judgment about tolerable rate, both considered prior to performing test of controls audit procedures?

7. When you subdivide a population into two populations for attribute sampling, how do the two samples compare to the one sample that would be drawn if the population had not been subdivided?

8. How does the relationship between the tolerable occurrence rate and the upper occurrence limit (maximum deviation rate) affect the auditor’s decision concerning control risk assessment?

9. Define expected occurrence rate (expected population deviation rate) and tolerable occurrence rate, explaining how they are set and how they affect sample size.

10. Name and define three factors comprising overall audit risk.

Source:

Cabrera, M. E. (2015). Auditing Theory. 2017 C. M. Recto Avenue, Manila: GIC ENTERPRISES & CO., INC.

[Show Less]