Boston University TAX TAX 101 **computation is based on PHILIPPINES INCOME TAX LAW1. If the taxpayer is a seller of services, which of the following shall not form part of its cost of services?a. Salaries and suppliesb. Employee benefitsc. Depreciation and rental expensesd. Interest expense2. MCIT shall applies to which of the following domestic corporations?I. Proprietary educational instit

...[Show More]

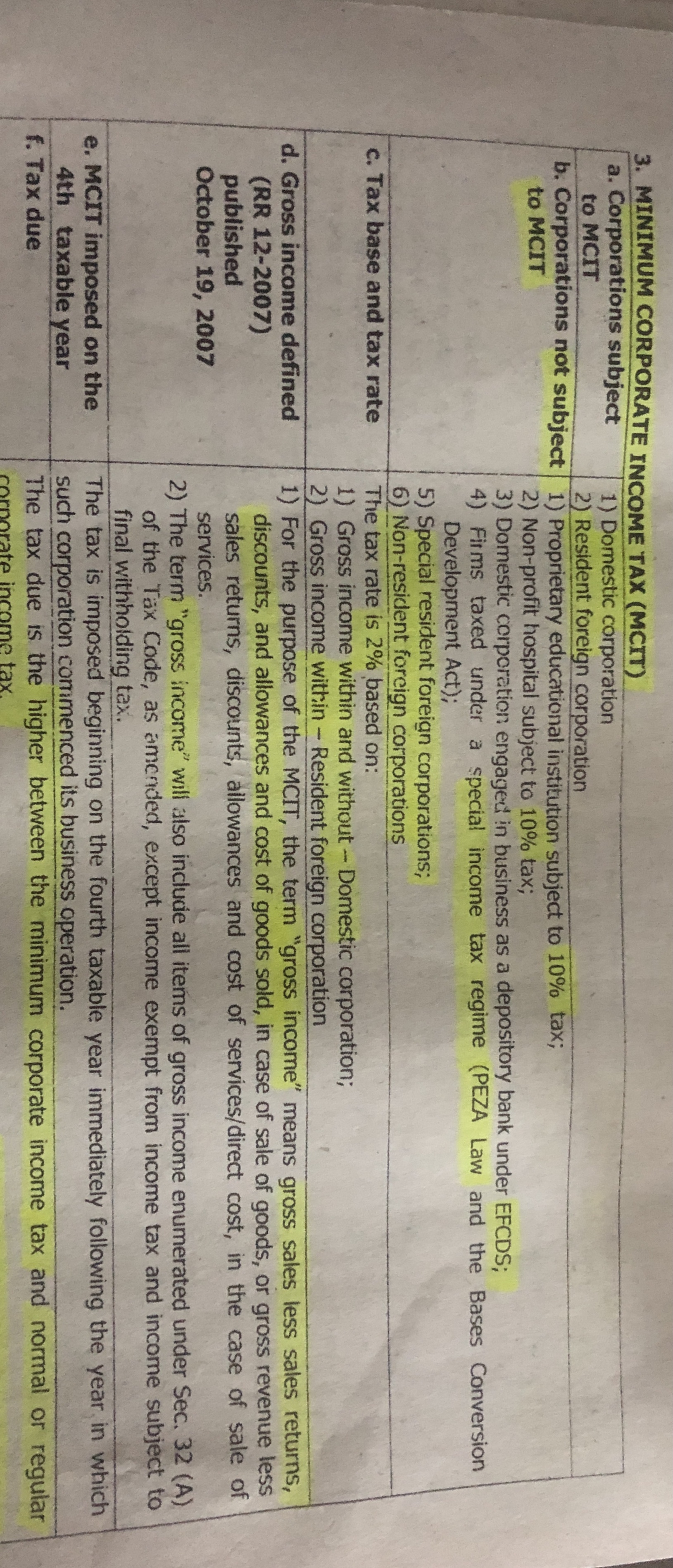

**computation is based on PHILIPPINES INCOME TAX LAW

1. If the taxpayer is a seller of services, which of the following shall not form part of its cost of services?

a. Salaries and supplies

b. Employee benefits

c. Depreciation and rental expenses

d. Interest expense

2. MCIT shall applies to which of the following domestic corporations?

I. Proprietary educational institutions

II. Non-profit hospitals

III. Depository banks under the expanded foreign currency deposit system (FCDS) on income from foreign currency

transactions with local commercial banks

IV. Firms that are taxed under a special income tax regime

a. I and II only c. All of the above

b. III and IV only d. None of the above

3. A PEZA registered enterprise has a registered and an unregistered activity. The MCIT shall apply to:

a. Registered activity

b. Unregistered activity

c. Both activities

d. Neither registered or unregistered activity

4. The following information were taken from the records of Tropikana Inc., a domestic corporation already in its fifth

year of operation:

Gross profit from sales P3,100,000

Capital gain on sale directly to a

buyer of shares in a domestic

corporation 100,000

Dividend from:

Domestic corporation 20,000

Resident foreign corporation 10,000

Interest on:

Bank deposit 20,000

Trade receivables 50,000

Business expenses 2,100,000

Income tax withheld 115,000

Quarterly income tax payments 160,000

Income tax payable prior year (10,000)

The income tax payable at the end of the year:

a. P318,000 c. P43,000

b. P63,200 d. P33,000

5. Short Time Services Inc., registered with BIR in 2013, has the following data for the year 2018:

Gross revenue P1,150,000

Discounts 100,000

Allowances 150,000

Salaries of personnel directly

involved in rendering service 300,000

Salaries of administrative personnel 100,000

Fees of consultants directly involved

in rendering service 50,000

Rental of equipment used in

rendering service 70,000

Rental of office space for use of

administrative personnel 50,000

Other operating expenses 420,000

How much was the income tax due and payable?

a. P27,000 c. P9,600

b. P6,600 d. Zero

6. Delta Corporation, already in its 5th year of operation as of 2019, has the following data:

2018 2019

Sales 1,700,000 2,300,000

Cost of Sales 1,050,000 1,425,000

Operating Expenses 675,000 480,000

The income tax payable in 2018 was -

a. P13,000 c. P35,000

b. P10,500 d. nil

7. The income tax payable in 2019 is -

a. P111,000 c. P98,000

b. P17,500 d. nil

Next four (4) questions are based on the following: Jolly Jeep Corporation has the following information for the taxable

year 2018:

QUARTER RCIT MCIT Creditable Withholding Tax

First 200,000 160,000 40,000

Second 240,000 500,000 60,000

Third 500,000 150,000 80,000

Fourth 300,000 200,000 70,000

Additional Information:

a) Excess MCIT for 2017, P60,000;

b) Excess tax credits from 2016 amounts to P20,000.

8. How much was the income tax payable for the first quarter?

a. P200,000 c. P120,000

b. P160,000 d. P80,000

9. How much was the income tax payable for the second quarter?

a. P660,000 c. P200,000

b. P460,00 d. P160,000

10. How much was the income tax payable for the third quarter?

a. P860,000 c. P600,000

b. P120,000 d. P140,000

11. How much was the annual income tax payable?

a. P1,260,000 c. P230,000

b. P390,000 d. P930,000

[Show Less]